Related Posts

Employers and Organizations

The 4 stages of competence: The Road to Financial Wellness

Last Update: November 18, 2015

Time and time again, money (and its management) is cited as one of the leading causes of stress. In various domains, including marital tension, qualitatively poorer college experiences and family strife, money can be found at the center of many conflicts. Outside of external economic hardship, exceptional life circumstances and sudden changes in employment status, many of the financial issues facing individuals comes down to behavior—the choices people are making with their money.

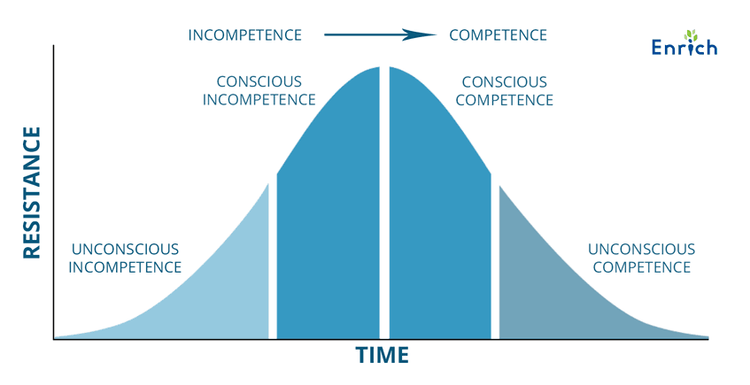

The 4 Stages of Competence, or the Conscious-Competence Model, is a framework for behavior change (Cannon, Feinstein & Friesen 2010) measured across two dimensions: Consciousness-Unconsciousness and Competence-Incompetence. The Conscious-Competence Model can be applied to various situations, particularly ones where individuals are not recognizing their behavior as problematic in the first place. As individuals pass through the four learning stages in the model, they are equipped with the skills necessary for success and are driven to use them.

Stage 1: Unconscious Incompetence

Many behavior change programs begin with the premise that if you do not see what is wrong with your behavior, you will never be motivated enough to change it. Unfortunately when it comes to making sound financial decisions, many people find themselves in this state.

Without taking the first steps to become financially literate, it is close to impossible for people to identify all the ways their money management decisions are hurting them. After the recession, unemployment rates were high, people’s living situations were in turmoil and many Americans went from working one full-time job to barely making ends meet with two or three part-time jobs.

There were still a number of people, however, who were not hit as hard by the recession who were still struggling to manage their bills. According to ABC News, the average American spends over $1,000 on coffee a year. In 10 years that is a down payment on a car or a good chunk of money to have set aside for emergencies or bills.

Stage 2: Conscious Incompetence

Conscious incompetence is the stage at which an individual recognizes the problem but is not taking or cannot see the proper steps to rectify it. If a person receives a bi-weekly salary that should cover bills and rent with some money left over, yet every Friday they find their bank account close to 0, the solution is simple: spend less money.

While avoiding buying coffee and preparing lunch instead of eating out are great first steps toward reaching financial goals, there are other areas where money can be saved that aren’t being addressed. Is the phone plan the most economic one to have? With a mobile data plan, is it necessary to bundle internet with a cable bill? Would it be cheaper to cancel cable and use a streaming service with a monthly subscription?

Ready to bring Enrich to your organization? Schedule a demo

Stage 3: Conscious Competence

Conscious competence is where a person has learned the skills necessary to avoid a financial problem, but in order to execute them they must be completely focused and aware of their chances to use them. Distractions such as increased stress, fatigue or just plain hunger can lead a person to act counter to their plan.

Limiting monthly expenses can be easy, but family birthdays and holiday celebrations can occur between one and four times a month. From a budgeting standpoint, there might not be holes where money is leaking out, but a night out or a family dinner can make light of a financial plan and undo all the good that was done in a less emotional state.

Stage 4: Unconscious Competence

Unconscious competence is the ultimate goal of any financial literacy program. The idea is to be so familiar with concepts and sound decision-making that when the opportunity presents itself, there is no second guessing. The right decision is made intuitively. That is not to say that people are not thinking critically about major purchases or financial decisions, but in a situation where interest rates on two car loans are separated by a significant number of points, the higher interest rate belonging to the more preferred car, a person will understand that in the long-term, appeasing the desire for that car is not in the best interest of the financial plan.

The right decision is made, but the utility and function of the purchase is still fulfilled.

Conclusion

The Conscious Competence Model is not a quick fix or a magic spell. It is used in a variety of contexts to direct individuals through the learning process. Reaching financial goals is about breaking old habits—often behaviors we have reinforced and used for many years—and replacing them behaviors that can lead to more positive outcomes.

When it comes to financial education, many of us find ourselves at Step 2, where we are aware of a behavioral deficit (making sound financial decisions) but aren’t quite sure where to start working on them. In this case we should never be discouraged; we are already on our way toward unconscious competence—mistakes are an integral part of the learning process. The priority should then be identifying which decisions could have been improved and not repeating them.

Featured Posts

Employers and Organizations

3 MIN

10 Simple Ways Benefits Managers Can Recession-Proof Their Employee Benefits Package

Employers and Organizations

3 MIN

3 Reasons to Make After-Tax Contributions to Your Retirement Plan

Employers and Organizations

4 MIN

Financial Information vs Employee Behavior Change: Which Is More Important for Your Company’s Financial Wellness Program?

Employers and Organizations

3 MIN

Does Your Employee Financial Wellness Program Take Mindset Into Consideration?

Related Posts

Employers and Organizations

7 MIN

Are Your Employees’ Behavior Biases Causing Them Financial Harm?

Employers and Organizations

4 MIN

Having More Money Does Not Mean Increased Financial Wellness

Employers and Organizations

3 MIN

3 Steps Employers Must Take to Create a Culture of Financial Wellness in the Workplace